TL;DR:

- Nebraska homeowners can sell quickly through cash buyers to avoid foreclosure and protect credit.

- Cash sales close in 7 to 14 days and require no repairs, unlike traditional sales.

- Verify legitimacy by requesting proof of funds, checking reviews, and comparing multiple offers.

Most Nebraska homeowners facing foreclosure assume their only path is months of stress, a damaged credit score, and an eventual auction. That assumption is wrong. Cash buyers close in 7 to 14 days, often well before the courthouse steps sale, giving you a real exit that protects your credit and puts money in your pocket. Nebraska's foreclosure process does give you a window to act, but that window closes faster than most people realize. This guide walks you through your options, how cash sales work, how to compare them honestly, and how to avoid the scams that prey on distressed homeowners.

Table of Contents

- Understanding foreclosure and your options in Nebraska

- How cash sales work: Fast relief for distressed Nebraska homes

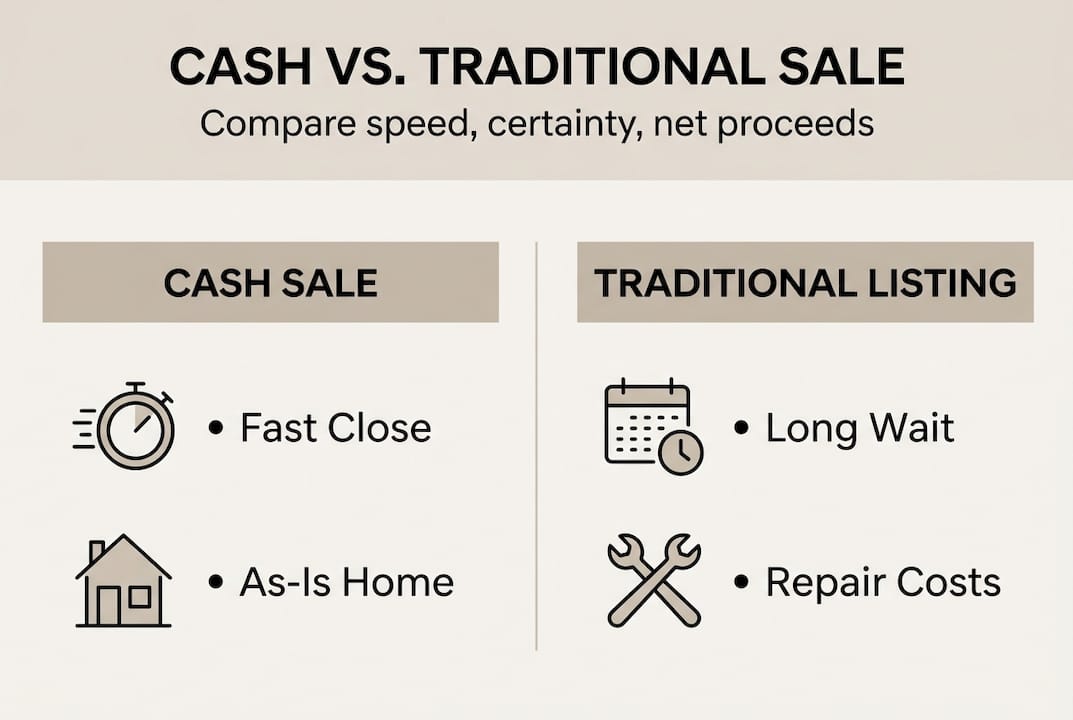

- Cash vs. traditional sale: Comparing speed, certainty, and net proceeds

- Protecting yourself: Choosing a legitimate cash buyer in Nebraska

- Why the 'fast cash equals less money' myth is misleading in Nebraska

- Need to sell fast? Get local Nebraska cash offer help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cash stops foreclosure fast | Cash buyers can close in as little as 7-14 days, helping you avoid auction and credit damage. |

| Net proceeds often similar | Despite offering below market, cash sales skip repairs, fees and delays, so your final payout can closely match traditional sales. |

| Choose buyers carefully | Verify legitimacy and review multiple offers to maximize your outcome and avoid scams. |

| Act early for more options | Respond quickly after default to keep your full range of solutions open before Nebraska's foreclosure deadline. |

Understanding foreclosure and your options in Nebraska

Nebraska uses a judicial foreclosure process, meaning the lender must go through the courts before selling your home at auction. That sounds slow, but the total timeline runs 6 to 9 months, with only 90 to 120 days between the notice of default and the scheduled auction. If you miss that window, your options shrink fast.

Here is a simplified look at what that timeline typically looks like:

| Stage | Approximate timeframe |

|---|---|

| Missed payments trigger default | Month 1 to 2 |

| Lender files lawsuit | Month 2 to 3 |

| Notice of default issued | Month 3 |

| Auction scheduled | Month 4 to 6 |

| Redemption period ends | Month 6 to 9 |

When you understand the Nebraska pre-foreclosure process, you can see clearly that the most powerful moves happen in the earliest stages. Waiting until month five leaves you with almost no leverage.

Your main options during this window include:

- Loan modification: Ask your lender to change the loan terms. This works if you have stable income and the lender is cooperative, but approval can take weeks.

- Short sale: Sell for less than you owe with lender approval. This takes longer than a cash sale and requires negotiation.

- Traditional listing: List with an agent and wait for a buyer. Realistic closing timelines run 60 to 90 days minimum, not counting time to find a buyer.

- Cash buyer: Sell as-is, skip repairs, close in 7 to 14 days, and stop the foreclosure process before auction.

For many homeowners in Lancaster, Douglas, and Sarpy counties, a cash sale is the only option that fits inside the available time window. Our fast sale guide breaks down what you need to do at each stage.

"The worst thing you can do in foreclosure is wait and hope something changes. Every week you delay narrows what you can actually do."

Pro Tip: Pull your foreclosure paperwork and note the auction date. Count backward from that date. If you have fewer than 60 days, a cash sale is likely your only realistic exit that protects your credit.

If you want a full breakdown of your choices based on timing, our guide on selling quickly in Nebraska walks through each scenario.

How cash sales work: Fast relief for distressed Nebraska homes

A cash sale sounds simple, but many homeowners are not sure what actually happens between the first phone call and the closing table. Here is the typical process from start to finish.

- Contact a cash buyer. Call or fill out a form online. A local buyer will usually respond within 24 hours.

- Property walkthrough or assessment. The buyer reviews the home, often in person. No staging, no cleaning, no repairs required.

- Receive a written offer. Most buyers provide a no-obligation offer within 24 to 48 hours of the assessment.

- Review and negotiate. You are not locked in. You can ask questions, push back on price, or decline entirely.

- Sign the purchase agreement. Once you accept, the paperwork is straightforward and typically handled by a local title company.

- Close and get paid. The title company processes the transaction, pays off your existing mortgage, and sends you the difference. Cash sales close in 7 to 14 days versus 60 to 90 days for a traditional sale.

The speed is not just a convenience. It is the mechanism that stops foreclosure. When the sale closes, the lender gets paid, the foreclosure case is dismissed, and the auction is canceled. Your credit takes a hit from the missed payments, but it avoids the far deeper damage of an actual foreclosure judgment.

Cash buyers also purchase homes completely as-is. That means no replacing the roof, no fixing the HVAC, and no negotiating repair credits. For a property in Lancaster County that needs real work, skipping repairs can save you tens of thousands of dollars you simply do not have during a financial crisis.

Pro Tip: Before signing anything, ask any cash buyer for written proof of funds. A legitimate buyer will provide a bank statement or letter from their financial institution without hesitation. If they stall or refuse, walk away.

Learn more about how cash offers help avoid foreclosure and what the process looks like for specific property conditions. You can also review distressed property solutions available specifically for Nebraska homeowners heading into 2026.

Cash vs. traditional sale: Comparing speed, certainty, and net proceeds

The most common objection to a cash sale is the price. "I'll get more listing it traditionally." Sometimes that is true on paper. But the real question is what you actually net after everything is said and done.

| Factor | Cash sale | Traditional listing |

|---|---|---|

| Time to close | 7 to 14 days | 60 to 90 or more days |

| Repairs required | None | Often $5,000 to $30,000+ |

| Agent commissions | None | Typically 5 to 6% |

| Closing costs | Often covered by buyer | 2 to 3% of sale price |

| Risk of deal falling through | Very low | 64% financing failures possible |

| Credit protection | High if closed before auction | Lower if process drags |

Let's run a quick real-world example. Say your Omaha home is worth $200,000 in good condition but needs $20,000 in repairs. A traditional buyer offers $190,000. After a 6% agent commission ($11,400), $4,000 in closing costs, and $20,000 in repairs, your actual net lands around $154,600. A cash buyer offers $160,000 as-is with no fees. Your net is $160,000. The cash offer wins.

Not every situation breaks that way, but the math is worth doing before you assume the traditional route is better. Our step-by-step home selling guide includes a worksheet to help you run these numbers for your specific property.

The other risk factor people underestimate is deal fall-through. Traditional buyers rely on financing, which can collapse at the last minute. If you are 60 days away from auction and your buyer's loan falls through, you are out of time and out of options.

"A slightly lower number that actually closes is worth more than a higher number that might not."

Protecting yourself: Choosing a legitimate cash buyer in Nebraska

Not every company that calls itself a cash buyer actually has cash. Some are wholesalers who plan to assign your contract to a third party without disclosing that upfront. Others use pressure tactics to push you into a below-market deal when you have more time and options than they want you to know about.

Here is how to protect yourself:

- Request proof of funds immediately. Ask for a bank statement or funding letter dated within the last 30 days. A real buyer will provide it.

- Check Google reviews and the Better Business Bureau. Look for local buyers with real reviews from Nebraska homeowners, not generic testimonials.

- Ask how long they have operated in Nebraska. Local buyers with years of experience in Lancaster, Douglas, and Sarpy counties understand the market and are more likely to close.

- Get multiple offers. Never accept the first offer you receive. Legitimate cash buyers encourage you to compare because they are confident in their value.

- Read the contract carefully. Look for assignment clauses that let the buyer transfer your contract to someone else. If you see one and they cannot explain it clearly, that is a red flag.

Watch for these specific warning signs:

- No physical address or local office

- Pressure to sign within hours

- Refuses to provide proof of funds

- Offer changes significantly at closing

- Cannot name a local title company they work with

Pro Tip: A trustworthy buyer will never pressure you to decide immediately. If someone tells you the offer expires in a few hours, that is a sales tactic, not a real deadline.

Our guide on finding legitimate cash buyers covers this in more detail. If you are in the Omaha area specifically, you can also review Omaha reputable cash buyers to understand what a credible local offer looks like.

Why the 'fast cash equals less money' myth is misleading in Nebraska

The assumption that a cash sale always means leaving money on the table is one of the most persistent and damaging myths homeowners in foreclosure carry into the process. We have seen it cost people real options.

Here is what that belief ignores: every day your home sits on the market costs you money. Property taxes accrue. Utilities run. If the lender has already started foreclosure proceedings, attorney fees pile up. And if the home needs repairs before it can list, you either pay out of pocket or accept a lower price anyway.

When you actually reverse-engineer the math on a typical distressed home in Omaha or Lincoln, net proceeds are often similar between cash and traditional sales after all costs are factored in. The cash route simply gets you there faster and with far less uncertainty.

Stress has a cost too. The weeks of showings, open houses, inspection negotiations, and lender delays take a toll that does not show up in a spreadsheet but is very real. The 2026 Nebraska market outlook shows continued inventory pressure, meaning distressed homes that need significant work face longer days on market, not shorter ones.

Our honest advice: do not compare a cash offer to the Zillow estimate on your home. Compare it to what you will realistically net after repairs, fees, time, and risk. That number is almost always a lot closer than it first appears.

Need to sell fast? Get local Nebraska cash offer help

If you are facing foreclosure or carrying a distressed property in Lancaster, Douglas, or Sarpy County, the clock is already running. You do not need a perfect home or months of preparation to move forward.

At Enko Home Buyers, we buy off-market homes across Nebraska as-is, no repairs, no agent fees, and no drawn-out timelines. We work specifically with homeowners who need speed and certainty. You can sell your house in foreclosure without waiting for the bank to decide your fate. When you are ready for a real number on your property, get a cash offer in Nebraska with no obligation. One conversation can tell you exactly where you stand.

Frequently asked questions

How fast can I sell my Nebraska home for cash if I'm in foreclosure?

Most cash buyers in Nebraska can close in 7 to 14 days, usually well before the foreclosure auction deadline, giving you time to stop the process and protect your credit.

Will I get less money selling for cash instead of listing traditionally?

You may see a lower sale price, but after agent fees, repairs, and the real risk of financing fall-throughs, your actual net is often very close to what a traditional sale would deliver.

How do I know if a cash buyer is legitimate in Nebraska?

Always ask for proof of funds, check local reviews, and get multiple offers from different companies before signing anything with any buyer.