TL;DR:

- Nebraska's foreclosure timeline creates urgent deadlines, often only 90 to 180 days to act.

- Quick sales to cash buyers or investors are the best options to avoid foreclosure and protect equity.

- Acting early and decisively is crucial; waiting reduces options and increases the risk of losing your home.

Most people assume Nebraska homes sell quickly because the market is hot. That's only part of the story. For thousands of homeowners in Lancaster, Douglas, and Sarpy counties, the real driver is something far more urgent: a legal clock that starts ticking the moment you miss a mortgage payment. Pre-foreclosure creates hard deadlines that no amount of market optimism can erase. If you're behind on payments or already received a default notice, understanding what's actually pushing your timeline is the first step toward making a smart, informed decision before your options run out.

Table of Contents

- How Nebraska's foreclosure timeline creates urgency

- Top reasons homes sell quickly in Nebraska

- Quick home sale options: What Nebraska homeowners need to know

- Common pitfalls and how to avoid them when selling fast

- Our take: The real secret behind fast home sales in Nebraska

- Discover your fastest way out of pre-foreclosure

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Foreclosure creates urgency | Nebraska's legal timeline forces quick action from distressed homeowners. |

| Several sale options | Owners can consider cash buyers, short sales, or auctions depending on timing. |

| Avoid common mistakes | Verifying buyers and acting early helps protect your credit and finances. |

| Lender approval matters | Short sales and bankruptcy pauses require lender cooperation to proceed. |

How Nebraska's foreclosure timeline creates urgency

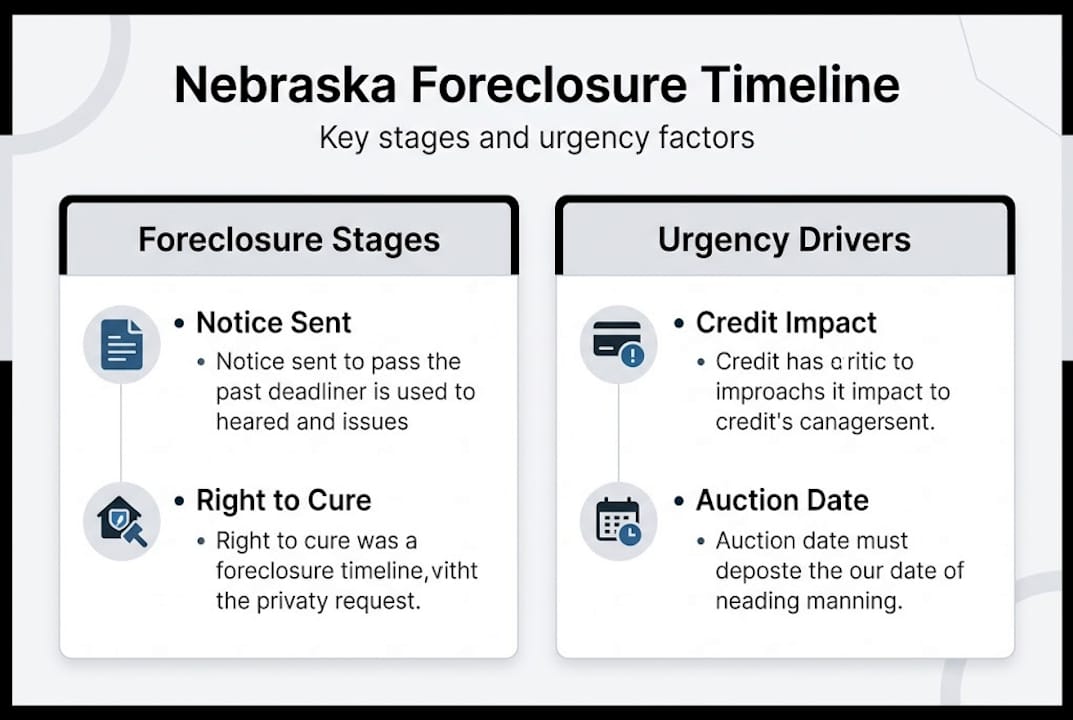

Nebraska uses a judicial foreclosure process, which means the lender must go through the courts to take your home. That might sound like it gives you more time, but the reality is more complicated. Once you miss payments, the lender files a notice of default. From there, a strict sequence of events begins, and each step shortens the window you have to act.

The Nebraska foreclosure process moves through several stages: the notice of default, a right-to-cure period, a court judgment, and finally a public auction. Each stage has its own deadline. Miss one, and you lose options that were available just weeks before.

Here's a simplified look at how the timeline typically unfolds:

| Stage | Approximate timing |

|---|---|

| Missed payment | Day 1 |

| Notice of default filed | 30 to 90 days after missed payment |

| Right-to-cure period | 30 days after notice |

| Court judgment | 60 to 90 days after filing |

| Public auction scheduled | 90 to 180 days from default notice |

The 90 to 180 day window from default notice to auction is your real operating window. It sounds like a lot of time, but it disappears fast once you factor in finding a buyer, negotiating, and closing.

This is why the step-by-step Nebraska guide we put together focuses so heavily on acting early. The homeowners who come to us with 60 or more days left have real choices. Those who wait until 10 days before auction are often left with almost none.

Understanding selling before auction is not just about speed. It's about preserving your credit, your equity, and your dignity. A foreclosure on your record can follow you for seven years. A pre-foreclosure sale, handled correctly, can protect all three.

Pro Tip: Even after you receive a notice of default, you still have time. But every week you wait shrinks your options. Start exploring your choices the same week you get that notice, not the week before the auction.

Top reasons homes sell quickly in Nebraska

Once you understand the timeline, the reasons behind fast pre-foreclosure sales become obvious. But there are more factors at play than just legal deadlines.

Financial pressure is the most immediate driver. A foreclosure doesn't just take your home. It destroys your credit score, sometimes by 100 to 150 points, and makes it harder to rent, borrow, or buy again for years. Selling before the auction date lets you walk away with some control over the outcome.

Legal deadlines create a hard stop that the traditional real estate market simply doesn't have. A typical home sale can take 60 to 90 days from listing to closing. In pre-foreclosure, you may not have that luxury. That's why cash buyers and investors become so attractive. They can close in 7 to 14 days.

Investor demand in Nebraska, especially in Lancaster, Douglas, and Sarpy counties, is strong. Buyers actively look for distressed properties that need work and can be purchased at a discount. That demand works in your favor when you need to move fast. There's a ready market for homes in exactly the condition yours might be in right now.

Here are the main triggers that push distressed Nebraska homeowners toward a fast sale:

- Avoiding a foreclosure record on their credit history

- Meeting a court-imposed auction deadline

- Stopping accumulating late fees and legal costs

- Releasing the emotional and financial stress of uncertainty

- Preserving any remaining equity before the bank takes it

The reasons distressed owners sell fast almost always come back to one thing: control. A fast sale, even at a discount, puts you in the driver's seat. A foreclosure auction does not.

It's also worth noting that what drives a quick sale in Nebraska isn't always desperation. Sometimes it's clarity. Homeowners who understand their options and act decisively often walk away in a far better position than those who wait and hope the situation resolves itself.

As noted in Nebraska foreclosure law, post-notice sales are possible until the auction date, but lender approval is required if the sale is a short sale. Bankruptcy can pause the process temporarily, but it doesn't erase the underlying debt.

Quick home sale options: What Nebraska homeowners need to know

Knowing what's driving these quick sales, here are your main options and what each one actually means in practice.

| Option | Typical timeline | Best for | Key requirement |

|---|---|---|---|

| Traditional listing | 60 to 90 days | Homeowners with time | Agent, repairs, showings |

| Cash buyer/investor | 7 to 21 days | Urgent pre-foreclosure | As-is condition accepted |

| Short sale | 60 to 120 days | Owed more than home value | Lender approval required |

| Foreclosure auction | Set by court | Last resort | No seller control |

Each option carries trade-offs. A traditional listing might get you a higher price, but it requires time, repairs, and a buyer who can secure financing. In pre-foreclosure, that timeline often doesn't work.

A cash sale to an investor is the fastest route. No repairs, no showings, no waiting for a bank to approve a buyer's loan. You get a firm offer and a closing date you can count on. For homeowners in Lancaster, Douglas, and Sarpy counties, home buying companies that specialize in distressed properties understand exactly what you're facing.

A short sale is an option when you owe more than the home is worth. The lender agrees to accept less than the full loan balance. It takes longer and requires lender cooperation, but it can prevent a full foreclosure from hitting your record.

Here's a simple process for evaluating your options:

- Calculate how many days remain before your auction date

- Contact your lender to understand what they will and won't approve

- Get a cash offer from a reputable buyer to establish a baseline

- Compare that offer against what a quick traditional listing might yield

- Make a decision based on your timeline, not your ideal outcome

For a broader look at distressed property solutions in Nebraska, the landscape in 2026 still favors sellers who act early and understand their leverage.

As Nebraska law confirms, bankruptcy can pause the foreclosure process temporarily, but it's not a long-term solution. It buys time, not resolution.

Pro Tip: Call your lender before you sign anything. Whether you're pursuing a short sale or a cash sale, your lender needs to be in the loop early. Surprises at closing can kill deals and cost you precious days.

Common pitfalls and how to avoid them when selling fast

Selling quickly comes with unique risks. Here's how to protect yourself and your home.

The biggest mistake distressed homeowners make is waiting. Every week you delay narrows your options and increases the chance that the auction date locks in before you can act. The second biggest mistake is trusting unverified buyers who promise fast cash but disappear when it's time to close.

Watch for these red flags when evaluating buyers:

- No proof of funds or financing

- Pressure to sign contracts immediately without review time

- Requests for upfront fees before closing

- Vague or verbal-only offers with no written contract

- Buyers who won't provide references or a track record

Fraud targeting pre-foreclosure homeowners is real. Scammers look for people under pressure who may not read contracts carefully. Always verify that any buyer is legitimate before signing anything.

Misunderstanding short sale rules is another common trap. Many homeowners assume that agreeing to a short sale means the lender will automatically approve it. They won't. The lender must review and approve the sale price, the buyer, and the terms. As Nebraska law makes clear, lender approval is required for any short sale, and the process can take months.

For homeowners dealing with selling inherited property in addition to their own financial stress, the complexity multiplies. Get legal advice early.

The Nebraska home selling resources we've compiled cover many of these scenarios in detail. Knowledge is your best protection against making a rushed, costly mistake.

Pro Tip: Before signing any contract, consult with your lender and ideally a real estate attorney. A 30-minute consultation can save you from a decision that costs you thousands or delays your sale past the auction date.

Our take: The real secret behind fast home sales in Nebraska

Most articles about quick home sales focus on pricing strategy or market conditions. That's useful advice in normal circumstances. But for homeowners in pre-foreclosure, it misses the point entirely.

In our experience working with distressed homeowners across Lancaster, Douglas, and Sarpy counties, the sellers who come out ahead are not the ones who got the highest offer. They're the ones who aligned their sale strategy to their foreclosure deadline rather than waiting for a perfect market moment.

The uncomfortable truth is that time, not price, is your most valuable asset in pre-foreclosure. Every day you spend chasing a higher number is a day closer to losing all control over the outcome. A cash offer at a discount, closed before the auction, is almost always a better result than a foreclosure on your record.

We've seen homeowners turn down solid cash offers hoping for something better, only to run out of time. We've also seen owners act quickly, close in two weeks, and walk away with enough to start fresh. The difference was almost never the offer. It was the decision to act.

If you want a deeper look at how this plays out in practice, the in-depth Nebraska quick sale guide walks through real scenarios that might mirror your own.

Discover your fastest way out of pre-foreclosure

If you're facing a foreclosure deadline in Nebraska, the worst thing you can do is wait for clarity that may never come. The best thing you can do is get a real offer from a real buyer and make an informed decision with actual numbers in front of you.

At Enko Home Buyers, we buy homes as-is in Lancaster, Douglas, and Sarpy counties. No repairs, no agent fees, no waiting. We specialize in distressed properties and understand exactly what you're up against. Whether you need to sell your Nebraska home fast or you're exploring options for a selling rental property situation, we can give you a no-obligation cash offer and a clear timeline. Reach out today and know your options before the clock runs out.

Frequently asked questions

How long do I have to sell my home after receiving a foreclosure notice in Nebraska?

You typically have 90 to 180 days from the notice of default before the property goes to auction. Acting early in that window gives you the most options.

Is it possible to sell my house after the foreclosure process has started?

Yes, you can often sell until the auction date, but lender approval is required for a short sale. A cash sale to an investor typically doesn't require lender approval if you're not underwater on the loan.

What are my options for selling my home quickly if I'm behind on payments?

Your main options are selling to a cash buyer, pursuing a short sale with lender approval, or listing with an agent. Cash buyers are fastest, often closing in under three weeks. Lender approval is required for short sales.

Can bankruptcy stop a Nebraska foreclosure?

Filing for bankruptcy can temporarily pause the foreclosure process through an automatic stay, but it is not a permanent fix and does not eliminate the underlying mortgage debt.

Recommended

- Sell your Nebraska home fast: step-by-step 2026 guide

- Fast home sales in Nebraska: guide for distressed owners

- Blog | Enko Home Buyers | Nebraska Home Selling Resources

- Sell House in Foreclosure Nebraska | Stop Foreclosure Fast | Enko Home Buyers

- Foreclosure Cold Calling Practice — AI Roleplay for Real Estate Investors & Wholesalers