TL;DR:

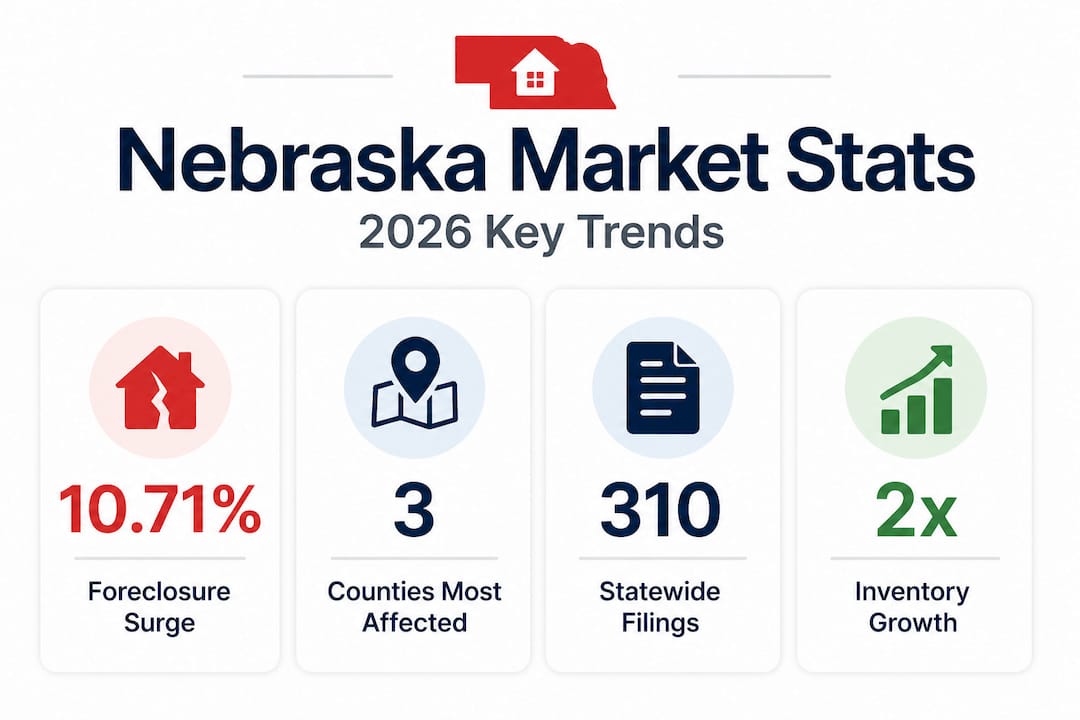

- Foreclosure filings in Nebraska increased by 10.71% in early 2026, mainly in populous counties.

- Rising foreclosure rates can lead to neighborhood value declines and increased distressed property sales.

- Early action by homeowners and landlords is crucial to protect equity and financial stability.

Nebraska has quietly crossed a threshold most homeowners and landlords haven't noticed yet. Foreclosure filings rose 10.71% year-over-year in Q1 2026, touching 310 properties statewide, and the pressure is concentrated in exactly the counties where most people live, work, and invest. If you own property in Lancaster, Douglas, or Sarpy County, or if you're a landlord managing rentals in the Omaha or Lincoln metro areas, what happens next in this market isn't just an abstract number. It's your equity, your cash flow, and your financial future on the line.

Table of Contents

- Why real estate market trends matter in Nebraska

- Key market trends in Lancaster, Douglas, and Sarpy counties

- How shifting market trends affect homeowners and landlords

- Foreclosure process and relief options in Nebraska

- What most Nebraska homeowners miss about market trends and risk

- Take control: sell fast, avoid risk, or learn more

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Foreclosure filings rising | Nebraska's foreclosure rate climbed 10.71% in the past year, impacting owners and landlords. |

| Act early for options | Proactive steps give distressed homeowners and landlords the best chance to preserve equity or avoid legal stress. |

| Local market trends differ | Trends in Lancaster, Douglas, and Sarpy counties can be more severe than the statewide average. |

| Multiple relief resources | Homeowners at risk can access HUD counseling, loan modifications, and quick sale solutions. |

Why real estate market trends matter in Nebraska

When real estate professionals talk about "market trends," they mean the measurable signals that show where a local housing market is heading. These signals include median sale prices, days on market, active inventory levels, and foreclosure filing rates. Together, they paint a picture of whether sellers have power, buyers have leverage, or distressed owners are running out of time.

Nebraska's overall numbers look calm on the surface. The state's foreclosure rate sits at 1 in 2,785 housing units, placing it 42nd nationally, which sounds reassuring. But that statewide average masks significant stress happening at the county level, particularly across Lancaster, Douglas, and Sarpy. A state ranking doesn't protect you from your specific neighborhood's pricing pressure or your specific lender's timeline.

Here's why those trends matter for real decision-making:

- Sale prices tell you whether selling now gives you breathing room or locks in a loss

- Pace of sales (days on market) shows you how fast you can realistically exit if needed

- Inventory levels indicate competition from other sellers, including distressed ones

- Foreclosure filing rates signal how many neighbors are in trouble, which pulls down neighborhood values

"A low statewide foreclosure ranking can give property owners false confidence. What matters is the trend direction, not just the snapshot number. Nebraska's 10.71% year-over-year increase tells a very different story than the rank alone."

For investors hunting for Nebraska distressed property outlook opportunities, a rising filing rate opens doors. For homeowners already stretched thin by mortgage payments, rising filings in your zip code are a warning. Either way, ignoring the data costs you.

| Market signal | What it tells you | Why it matters |

|---|---|---|

| Foreclosure filing rate | Financial stress in the market | Predicts price pressure and distressed inventory |

| Days on market | Buyer demand vs. supply | Affects how fast you can sell |

| Median sale price | Current market value | Determines equity position |

| Active inventory | Competition level | Shapes negotiating power |

The bottom line is this: market trends are not background noise. They are the operating environment every property owner in Nebraska is working inside right now, whether they realize it or not.

Key market trends in Lancaster, Douglas, and Sarpy counties

These three counties are the economic engine of Nebraska. They contain Omaha, Lincoln, Bellevue, and Papillion, and together they represent the overwhelming majority of the state's housing activity. What happens here sets the tone for the broader market.

Lancaster, Douglas, and Sarpy saw a sharp jump in foreclosure filings in March 2026, a trend that has continued into Q2. This is not a blip. It reflects cumulative financial strain from rising interest rates, higher property taxes, and increased cost of living that has been building since 2023.

Here's how the counties compare right now:

| County | Key city | Foreclosure trend | Inventory level | Market pressure |

|---|---|---|---|---|

| Lancaster | Lincoln | Rising filings, Q1 spike | Tightening | Moderate to high |

| Douglas | Omaha | Highest volume of filings | Slightly elevated | High |

| Sarpy | Bellevue/Papillion | Rising from a low base | Tight | Moderate |

What the numbers mean for you:

For sellers, more foreclosure filings in your county means more distressed properties hitting the market, which pulls comparable sale prices downward. If you wait too long to list, you're competing against homes priced at distressed levels that lenders are eager to offload quickly.

For landlords, a rising foreclosure rate often correlates with tenant instability. Renters who were previously homeowners get displaced, which can boost short-term rental demand, but it also signals a fragile local economy that can shift vacancy rates fast.

For investors, this is exactly the environment that creates actionable opportunities. Understanding pre-foreclosure factors in Nebraska allows buyers to identify motivated sellers before a property ever hits the open market.

The top trends shaping these counties right now:

- Foreclosure filings accelerated sharply in March 2026 across all three counties, with Douglas County leading in raw volume

- Inventory remains historically tight, meaning properties that are priced right still move quickly

- Median home prices have held relatively steady but are showing softening in neighborhoods with clustering distressed sales

- Days on market have ticked upward for homes priced above local median, reflecting buyer caution

- Investor activity in off-market deals has increased as sophisticated buyers position ahead of further distress

Pro Tip: If you're a landlord or homeowner in one of these counties and haven't reviewed comparable sales in your specific zip code in the last 90 days, you're making decisions with outdated information. Local trends within these counties can vary dramatically by neighborhood.

How shifting market trends affect homeowners and landlords

Let's make this concrete. Imagine a homeowner in Lincoln who bought in 2020 at $230,000, currently owes $195,000, and the home's current market value is approximately $260,000. On paper, there's about $65,000 in equity. That sounds safe. But if foreclosure filings keep rising and distressed comps start pulling that market value down by even 8%, that equity shrinks by roughly $20,000 in a matter of months. Time is not neutral in a trending market.

For homeowners at risk, the core dangers are:

- Assuming rising filings won't affect their specific property value

- Waiting for the "right moment" to sell while equity quietly erodes

- Not contacting their lender at the first missed or at-risk payment

- Missing the narrow window between pre-foreclosure and public filing

For landlords, the risks stack differently. Underperforming rentals in an area with rising foreclosures face double pressure. Vacancy rates can climb as would-be tenants choose distressed homes for sale instead of renting. Meanwhile, the landlord still carries the mortgage, insurance, maintenance, and property tax burden. A rental that breaks even in a stable market can turn cash-flow negative fast.

Nebraska law gives lenders tools to move quickly once a borrower falls behind. Nebraska judicial foreclosure takes 5-7 months from filing to sale, with no post-sale redemption period. Options like HUD counseling, loan modification, and bankruptcy exist, but each one has a window. Miss the window, and your options narrow dramatically.

Your realistic options if you're at risk:

- HUD-approved housing counseling: Free, confidential, and often the fastest way to understand your specific situation

- Loan modification: Ask your lender to restructure the loan terms before a filing is initiated

- Short sale: Sell the property for less than owed, with lender approval, before foreclosure is filed

- Cash sale to a direct buyer: Often the fastest exit with the least damage to your credit

Read the Nebraska home selling guide for a detailed breakdown of each exit path. If you're already in the process, understanding your rights around selling a home in foreclosure can still preserve a significant portion of your equity.

Pro Tip: The moment you miss a payment or know you're about to, call your lender the same week. Lenders have more internal flexibility to work with borrowers before a formal default notice is filed than most homeowners realize. Silence is the single most expensive choice in this situation.

Foreclosure process and relief options in Nebraska

Nebraska operates on a judicial foreclosure model. That means lenders must go through the court system to repossess a property, which gives homeowners more visibility into the process and more time to act. Here's how the timeline typically unfolds:

- Missed payment: Lender begins internal collection processes, usually within 30-60 days of the first missed payment

- Notice of default: Formal written notice sent to the borrower, typically after 90 days of non-payment

- Filing with the court: Lender files a petition with the county court to begin foreclosure proceedings

- Summons served: Homeowner is formally notified of the lawsuit and given a deadline to respond

- Judgment: If no resolution is reached, the court enters judgment in the lender's favor

- Sheriff's sale: Property is auctioned publicly, usually within a few weeks of judgment

- Sale confirmed: Court confirms the sale, and ownership transfers

This full process spans 5-7 months from filing to sale, depending on the county court's docket and whether the homeowner contests or engages in the process. Nebraska does not offer a post-sale redemption period, meaning once the sale is confirmed, there's no legal path to reclaim the property.

"Most homeowners wait until stage 4 or 5 to take serious action. By then, they've lost half the available options and most of their negotiating leverage. The first two stages are where the real power sits."

Relief options worth knowing:

- NIFA (Nebraska Investment Finance Authority): Offers homeowner assistance programs for those facing hardship

- HUD-approved counselors: Available at no cost and can negotiate directly with your lender

- Chapter 13 bankruptcy: Creates a court-supervised repayment plan that can pause foreclosure while you restructure debt

- Loan forbearance: A temporary pause or reduction in payments while you stabilize your finances

- Nebraska homestead exemption: Protects up to $60,000 of home equity from certain creditors, though this does not stop a mortgage foreclosure by your primary lender

The guide for distressed Nebraska homeowners walks through each option with more detail. And if a fast sale is the cleanest exit, the quick sale guide for distressed properties explains what that process looks like from first contact to closing.

Pro Tip: Your maximum leverage is in the first 60-90 days after you realize you're in trouble. Every week you wait narrows the gap between what you owe and what your options cost. Early action almost always means more money in your pocket at the end.

What most Nebraska homeowners miss about market trends and risk

Here's the uncomfortable truth that most local advisors won't say directly: Nebraska's reputation as a stable, Midwestern real estate market has become a liability for many property owners. That reputation creates a psychological buffer that delays action precisely when speed matters most.

People here see the national headlines about coastal foreclosure spikes and assume they're insulated. But insulation is relative and temporary. A 10.71% year-over-year increase in filings doesn't sound catastrophic until you realize it's compounding. If the same rate continues for two more quarters, you're looking at a fundamentally different market than the one most current owners bought into.

The subtler danger is what we call "trend drift," where small shifts in filing rates, inventory, or pricing move slowly enough that no single month feels alarming. But six months of drift can erase 10-15% of a neighborhood's comparative value as distressed sales redefine what buyers are willing to pay.

For landlords, this is especially punishing. An underperforming rental in a neighborhood where distressed sales are stacking up is a problem that compounds quietly. The property loses rental appeal, maintenance costs don't drop, and the eventual sale price falls just as you need it most. Exploring problem property selling strategies early, before the stress becomes acute, almost always produces a better outcome than waiting for a crisis to force the decision.

The investors and homeowners who come out ahead in this environment are not the ones with the best properties. They're the ones who watched the data, recognized the pattern early, and moved while they still had choices. Clarity about what's happening in your specific county is the most valuable asset you can hold right now.

Take control: sell fast, avoid risk, or learn more

If you've read this far, you already know more about what's happening in Nebraska's housing market than most of your neighbors. That knowledge only protects you if you act on it.

Enko Home Buyers works directly with homeowners and landlords across Lancaster, Douglas, and Sarpy counties who need to move fast, whether that's because of foreclosure pressure, a rental that's draining cash, or an inherited property you don't want to manage. We buy homes as-is, no repairs needed, no agent commissions, no lengthy listing process. If you're ready to sell your Nebraska home fast, we can put a cash offer in your hands quickly. If you're managing a rental you're ready to exit, check out what we offer when you sell a rental property. We also work with families navigating inherited property situations who want a fast, fair resolution through cash for inherited property.

Frequently asked questions

Has Nebraska's foreclosure rate increased in 2026?

Yes, Nebraska filings rose 10.71% year-over-year in Q1 2026, reaching 310 properties statewide, with the sharpest increases concentrated in the state's most populated counties.

How long does foreclosure take in Nebraska?

A typical Nebraska judicial foreclosure takes 5-7 months from the initial court filing to the sheriff's sale, giving homeowners a meaningful window to pursue alternatives if they act early.

Are there relief options for Nebraska homeowners at risk?

Yes, relief options include HUD counseling, loan modification, forbearance, Chapter 13 bankruptcy, NIFA assistance programs, and direct cash sale to a buyer, each with different timelines and eligibility requirements.

Do Nebraska landlords face higher risks from recent market trends?

Rising foreclosure rates increase distressed inventory in local markets, which pressures rental demand and comparable values, making it critical for landlords in Lancaster, Douglas, and Sarpy to track neighborhood-level data, not just statewide averages.