TL;DR:

- Most Nebraska homeowners delay selling problem properties, risking increased costs and legal issues.

- Selling quickly can protect equity, reduce costs, and prevent foreclosure or further deterioration.

- Immediate action is recommended when facing liens, major repairs, inheritance, or imminent foreclosure.

Most Nebraska homeowners with a problem property believe that waiting will eventually pay off. Hold on a little longer, fix a few things, and the market will reward your patience. But for distressed homeowners in Lancaster, Douglas, and Sarpy counties, that belief often turns into months of mounting costs, legal exposure, and lost equity. The reality is that problem properties rarely get easier to manage with time. This guide breaks down what qualifies as a problem property in Nebraska, the real risks of holding on, and the specific triggers that signal it is time to sell, including edge cases like inherited homes, tax liens, and divorce settlements.

Table of Contents

- What makes a property "problematic" in Nebraska?

- Major risks of keeping a problem property

- Benefit analysis: Selling vs. holding onto a problem property

- When is selling the best solution? Nebraska-specific triggers

- The overlooked reality: Most Nebraska homeowners wait too long

- Ready to take the next step? Nebraska specialists can help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Nebraska-specific risks | Local rules and equity caps mean waiting can expose homeowners to bigger losses. |

| Cash sales offer speed | Selling for cash is often the fastest way out of legal or financial distress. |

| Act quickly if triggered | Foreclosure, liens, or major repairs in Nebraska signal it’s time to consider selling. |

| Know your exemption | The $120,000 homestead exemption protects only part of your home’s equity in bankruptcy. |

What makes a property "problematic" in Nebraska?

Not every home that needs work is a problem property. But when repairs, legal complications, or personal circumstances pile up together, a home can shift from an asset into a liability fast.

In Nebraska, problem properties typically fall into a few clear categories:

- Major structural or safety issues that require costly repairs before the home can be sold or rented

- Inherited homes that came through probate and may have back taxes, deferred maintenance, or title complications

- Properties with tax liens where unpaid property taxes have triggered a legal claim against the home

- Homes caught in divorce settlements where both parties need a clean financial break

- Rentals with problem tenants or code violations that have attracted city scrutiny

- Properties tied to relocation where the owner needs to move fast and cannot manage the home remotely

These situations are common across Lancaster, Douglas, and Sarpy counties. Omaha, Lincoln, and Bellevue all have active code enforcement programs, and a home that sits vacant or deteriorates quickly draws attention.

One factor that many Nebraska homeowners overlook is how the state's bankruptcy homestead exemption shapes their options. The Nebraska bankruptcy homestead exemption protects up to $120,000 of home equity if you file for bankruptcy. That sounds like a safety net, but it also means that if your equity exceeds $120,000, the portion above that threshold is exposed to creditors. For homeowners with a valuable but distressed property, this can tip the math toward selling rather than filing.

If you are navigating any of these situations, the distressed homeowner guide covers your options in plain terms. And if foreclosure is already a concern, understanding the pre-foreclosure factors specific to Nebraska can help you move before the situation worsens.

The bottom line is that a problem property is not just about the condition of the house. It is about the combination of the home's condition, your financial situation, and the legal complications attached to it.

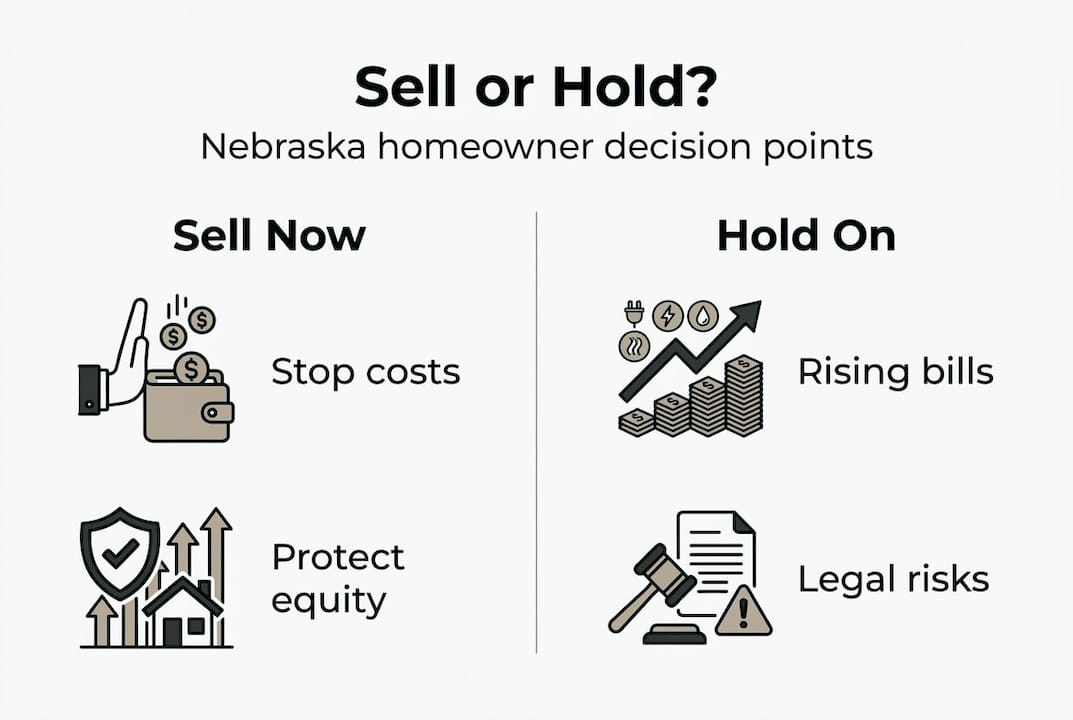

Major risks of keeping a problem property

Holding onto a problem property feels like the cautious choice. In practice, it is often the most expensive one.

Here are the top risks Nebraska homeowners face when they hold on too long:

- Ongoing carrying costs including property taxes, insurance, utilities, and maintenance that accumulate every month whether the home generates income or not

- Code violation fines from city inspectors in Omaha or Lincoln that can compound quickly on vacant or deteriorating homes

- Foreclosure acceleration where missed mortgage payments push the lender to begin legal proceedings, shrinking your options and timeline

- Lawsuit exposure from tenants, neighbors, or municipalities if the property causes injury or becomes a nuisance

- Declining market value as deferred maintenance makes the home harder to sell at a fair price over time

The Nebraska homestead exemption protects up to $120,000 of equity in bankruptcy. Homeowners with equity above that level risk losing the difference to creditors if they wait too long and finances deteriorate.

For many homeowners in Lancaster and Douglas counties, the equity in a distressed property is their largest financial asset. Letting that equity erode through carrying costs, fines, and declining value is a slow-moving financial loss that is easy to underestimate month to month.

Pro Tip: When you evaluate whether to keep a problem property, do not just add up the dollar costs. Factor in the hours you spend managing it, the stress of uncertainty, and the opportunities you are missing by having your capital tied up. Time has a real cost.

Homes with active tax liens or code violations also face increased scrutiny from local governments. Cities like Omaha have nuisance abatement programs that can force repairs or even demolition at the owner's expense. The distressed property solutions available in 2026 are broader than most homeowners realize, but they require acting before the situation escalates.

Benefit analysis: Selling vs. holding onto a problem property

Once you understand the risks, the comparison between selling and holding becomes much clearer. Here is a side-by-side look at the key outcomes for distressed Nebraska homeowners.

| Factor | Selling now | Holding on |

|---|---|---|

| Monthly costs | Stops immediately | Continues to grow |

| Legal exposure | Resolved at closing | Grows with each violation or missed payment |

| Equity protection | Locked in at sale | Erodes with time and costs |

| Emotional stress | Clean exit | Ongoing uncertainty |

| Repair burden | Buyer takes it on | Owner responsible |

| Foreclosure risk | Eliminated | Increases each month |

| Timeline control | You set it | Lender or court may decide |

The Nebraska homestead exemption is a useful data point here. If your home has more than $120,000 in equity, selling protects that full amount. Filing for bankruptcy would only shield the first $120,000. For homeowners with significant equity in a distressed property, a sale often preserves more wealth than any other option.

Pro Tip: Timing matters more than most people realize. Selling before a foreclosure filing appears on your record protects your credit and keeps more cash in your pocket. Every month you wait after missing payments narrows your options.

There are situations where holding makes sense. If the market is in a short-term dip and you have the financial cushion to wait, or if the home has genuine sentimental value and you can afford the carrying costs, holding is a reasonable choice. But for most distressed homeowners in Nebraska, those conditions do not apply. If you are considering an inherited property specifically, the selling an inherited home process in Nebraska has specific steps worth knowing. And if speed is your priority, the quick sale guide walks through how to move fast without leaving money on the table.

When is selling the best solution? Nebraska-specific triggers

Some situations call for a fast decision. In Nebraska, these are the clearest signals that selling is not just a good idea but an urgent one.

Key triggers for homeowners in Lancaster, Douglas, and Sarpy counties:

- You are 60 or more days behind on mortgage payments

- A tax lien has been filed against the property

- The home needs repairs that exceed 20% of its market value

- You inherited a property you do not want to manage

- You are relocating out of state and cannot manage the home remotely

- A divorce requires a clean financial split

- The property has been vacant for more than 90 days

Here is how those scenarios typically play out for Nebraska homeowners:

| Scenario | County most common | Best option |

|---|---|---|

| Behind on payments | Douglas, Lancaster | Sell before foreclosure filing |

| Tax lien filed | All three counties | Cash sale to clear lien at closing |

| Inherited unwanted property | Lancaster, Sarpy | Sell as-is, skip probate delays |

| Major repairs needed | All three counties | Cash buyer, no repair contingency |

| Relocation needed | Douglas, Sarpy | Fast close, flexible timeline |

| Divorce settlement | All three counties | Sell and split proceeds cleanly |

Nebraska law limits the homestead exemption to $120,000, and local courts in Douglas County move quickly on foreclosure cases. Sarpy County has seen increased vacancy enforcement in recent years, and Lincoln's code enforcement in Lancaster County has become more active on distressed properties.

Local rental market conditions also matter. If you are a tired landlord in Omaha or Bellevue and the rental market has softened, carrying a vacant property while waiting for a tenant costs more than most people budget for. The step-by-step sale guide lays out exactly how to move from decision to closing quickly in Nebraska.

If two or more of these triggers apply to your situation, a cash sale is likely your fastest path to financial stability.

The overlooked reality: Most Nebraska homeowners wait too long

After working with distressed homeowners across Lancaster, Douglas, and Sarpy counties, one pattern stands out clearly. Most people wait. They wait for a better market, for repairs to become affordable, for a situation to resolve itself. And while they wait, costs climb, options narrow, and stress builds.

The myth driving this behavior is that holding on is the financially responsible choice. For a move-in-ready home in a stable situation, that might be true. For a problem property with liens, violations, or legal complications, it almost never is.

Cash offers and fast sales get dismissed as low-ball deals. But when you subtract months of carrying costs, repair bills, and the risk of foreclosure from a traditional sale price, the gap between a cash offer and a retail sale shrinks considerably. What you gain is certainty, speed, and a clean exit. Those have real value that does not show up on a spreadsheet.

The examples of quick sales from Nebraska homeowners who acted early tell a consistent story. The ones who moved quickly kept more of their equity and moved on faster. The ones who waited often ended up with less.

Ready to take the next step? Nebraska specialists can help

If you recognized your situation anywhere in this guide, you do not have to figure out the next step alone. We buy problem properties across Lancaster, Douglas, and Sarpy counties, including homes in foreclosure, inherited properties, rentals, and homes that need significant work.

We make fair, no-obligation cash offers and close on your timeline. Whether you need to stop foreclosure fast, want to sell your rental fast, or simply want a straightforward Nebraska home cash sale, we are local, experienced, and ready to help you move forward. No repairs, no agent fees, no uncertainty. Just a clear offer and a clean close.

Frequently asked questions

Does the Nebraska $120,000 homestead exemption mean I can't lose my home?

The exemption protects up to $120,000 of equity in bankruptcy, but if you owe more than the home is worth or have equity above that limit, you may still be required to sell to satisfy creditors.

What types of properties do cash buyers in Nebraska purchase?

Cash buyers typically purchase homes in foreclosure, with tax liens, inherited properties, rentals, and homes that need major repairs, often buying them as-is with no conditions.

If I'm behind on payments, when should I think about selling?

The sooner you act, especially before a foreclosure filing appears on your record, the more financial options and equity you protect. Waiting even 30 days can reduce your choices significantly.

Do I need to repair my Nebraska property before selling for cash?

Most cash buyers purchase homes as-is, meaning you do not need to make any repairs before closing. The buyer takes on the property in its current condition.