TL;DR:

- Pre-foreclosure homes in Nebraska sell quickly, often within 30 to 60 days, due to legal and financial urgency.

- Investors actively monitor notices of default to secure off-market deals at discounts of 10 to 30 percent, facilitating fast closings.

- Early action by homeowners, such as selling privately, offers better equity recovery and minimizes credit impact compared to auction sales.

Pre-foreclosure homes in Nebraska can change hands in weeks, not months, catching many homeowners and investors by surprise. Foreclosure timelines are compressing nationally, with the average down to 592 days in Q4 2025, and Nebraska's own window sitting around 6 to 9 months total. That speed matters enormously if you are a homeowner trying to protect your credit and equity, or an investor hunting off-market properties at a real discount. This guide breaks down exactly what pushes Nebraska pre-foreclosures to close so quickly, what both sellers and buyers need to know, and how to use that urgency to your advantage.

Table of Contents

- Understanding pre-foreclosure and what makes these sales unique

- Key reasons pre-foreclosures sell so fast in Nebraska

- How investors drive fast pre-foreclosure sales

- Private sales vs auctions: speed, price, and the risks for sellers

- Why acting early in pre-foreclosure is your strongest move

- Need to sell fast? Nebraska pre-foreclosure experts can help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Act fast in pre-foreclosure | Speed is critical in Nebraska because tight timelines determine if you keep more equity. |

| Investor interest delivers cash | Cash buyers move fast, often closing in 7-21 days for urgent homeowners. |

| Auctions bring deeper discounts | Homes sold at auction typically net 20-40% less for owners, making early sales much more favorable. |

| Know your sale options | Direct private sales let you negotiate and preserve your credit compared to auctions or short sales. |

Understanding pre-foreclosure and what makes these sales unique

Pre-foreclosure is the period between a lender filing a Notice of Default (NOD) and the actual foreclosure auction. Think of it as a legal warning period. The homeowner still owns the property and can still control what happens next, but the clock is running. In Nebraska, this window typically lasts anywhere from 30 to 180 days depending on the lender, loan type, and how quickly legal proceedings move.

This phase is fundamentally different from foreclosure. In a foreclosure, the court or lender takes over. In pre-foreclosure, the seller keeps negotiating power. That distinction is huge. A homeowner who acts during this window can sell to a buyer at a price both parties agree on, pay off the mortgage, and walk away with something. A homeowner who waits loses that control entirely.

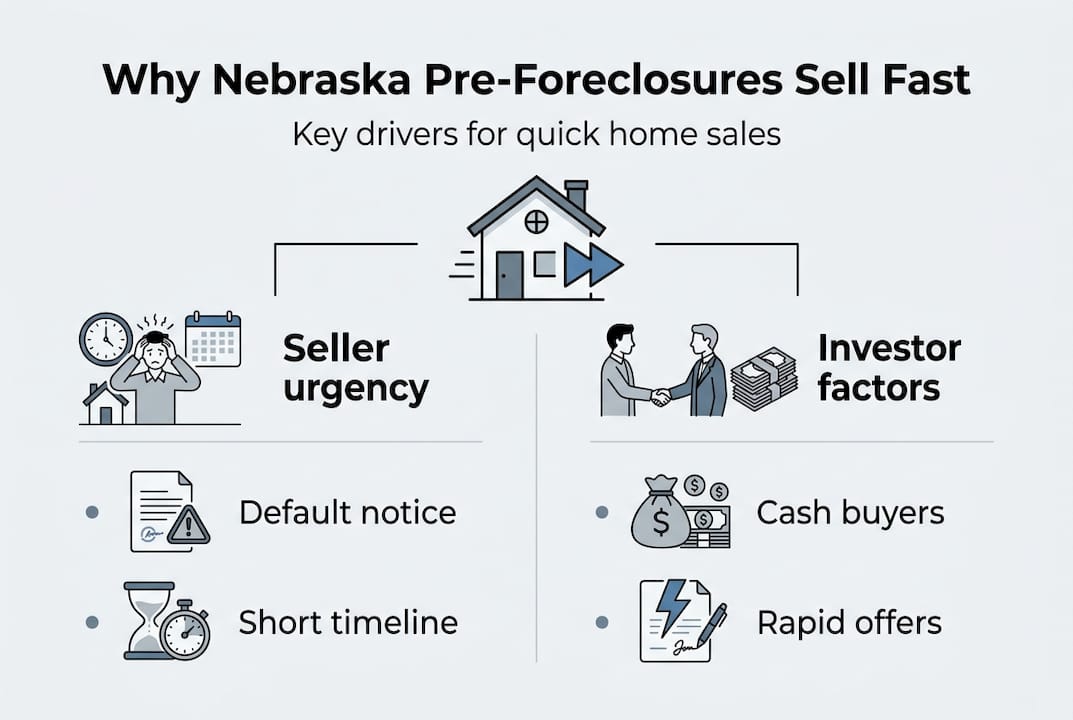

Several factors make pre-foreclosure factors in Nebraska push sales to happen faster than in a normal market:

- Legal pressure: The NOD starts a countdown. Every week of delay shrinks options.

- Financial urgency: Missed payments add up fast with fees and interest.

- Emotional weight: Homeowners want to resolve the situation and move forward.

- Investor demand: Cash buyers actively watch NOD filings and approach sellers directly.

- Credit protection: The homeowner's credit score is still saveable at this stage.

Statistic: Nebraska pre-foreclosure periods typically last just 30 to 180 days, making every week of inaction costly for sellers.

The speed also comes from a mindset shift. Once a homeowner receives a default notice, the game changes. They are no longer thinking about getting top dollar. They are thinking about getting out with the least damage. That shift in priority is exactly what accelerates deals.

Pro Tip: The earlier you take action after receiving a Notice of Default, the more leverage you have. Early sellers often recover more equity and have time to negotiate repairs or closing costs rather than accepting the first offer out of panic.

Pre-foreclosures sell fast primarily because homeowner urgency meets investor readiness in a very narrow legal window. That combination is rare in real estate and explains why these deals close at a pace that surprises most people new to distressed property sales.

Key reasons pre-foreclosures sell so fast in Nebraska

Nebraska's legal structure plays a direct role in how fast things move. The state uses a judicial foreclosure process, meaning the lender must go through the courts. While that sounds like it slows things down, it actually puts pressure on the homeowner to act fast. Nebraska judicial foreclosures take approximately 142 to 180 days total, with roughly 30 days after the notice of default to cure the loan before proceedings accelerate.

That 30-day window is short. For most homeowners already behind on payments, curing the loan means coming up with thousands of dollars immediately. Selling quickly becomes the realistic path.

Here is a look at how the timelines compare:

| Stage | Pre-foreclosure private sale | Auction timeline |

|---|---|---|

| Initial notice to offer | 7 to 30 days | N/A |

| Offer to closing | 7 to 21 days | Same day |

| Total process | 30 to 60 days | 142 to 180 days |

| Seller control | Full | None |

| Equity recovered | Moderate to high | Low |

Beyond the legal timeline, here are the core reasons Nebraska sellers move fast:

- Credit score risk: A completed foreclosure can drop a credit score by 100 points or more, affecting borrowing ability for years.

- Accumulating debt: Missed payments plus legal fees pile up every month.

- Deficiency risk: If the auction price does not cover the mortgage, the lender can pursue the homeowner for the difference.

- Emotional relief: Many sellers simply want the stress over.

"Waiting for the auction rarely makes financial sense for the homeowner. The damage compounds with every passing week."

For investors, selling fast in Nebraska distressed situations means jumping on deals before competing buyers appear. Public NOD records are accessible, so savvy buyers monitor filings in Lancaster, Douglas, and Sarpy counties regularly. Speed is a competitive advantage. The investor who contacts a seller in week two of default almost always beats the one who waits until week six.

If you are weighing your options as a seller, understanding distressed property solutions available in Nebraska can help you see which path protects the most equity. And if you are wondering about selling before auction, the short answer is: almost always yes, you should.

How investors drive fast pre-foreclosure sales

Investors are a major engine behind why pre-foreclosure sales close so quickly. They are not waiting for listings to appear on the MLS. They are pulling public NOD records, doing their research, and reaching out directly. This proactive approach collapses the typical listing-and-showing timeline into something that can happen in days.

Investors buy pre-foreclosures at 10 to 30% discounts for off-market deals needing renovation, with full property access and strong negotiation leverage. For a property worth $200,000 in Lancaster County, that might mean a cash offer of $150,000 to $175,000. The seller avoids foreclosure. The investor gets a property with built-in equity.

Here is how a typical investor-driven pre-foreclosure purchase unfolds:

- Investor identifies NOD through public records in Douglas, Lancaster, or Sarpy County.

- Direct outreach to the homeowner, often within days of the filing.

- Property walkthrough to assess renovation needs and calculate offer.

- Cash offer submitted, often within 48 to 72 hours of first contact.

- Contract signed and title search ordered immediately.

- Closing happens in as little as 7 to 21 days.

| Factor | Pre-foreclosure private sale | Auction purchase |

|---|---|---|

| Access to property | Yes, full walkthrough | Usually none |

| Price negotiation | Yes | No |

| Inspection possible | Yes | Rare |

| Closing speed | 7 to 21 days | Same day |

| Title clarity | Title search done | Title issues possible |

Pro Tip: Even in fast deals, never skip a title search. Pre-foreclosure properties sometimes carry liens from unpaid contractors, taxes, or second mortgages that can survive the sale and become your problem after closing.

For homeowners, the investor's urgency is actually a benefit. Finding cash buyers in Nebraska who are ready to close fast means you can stop the foreclosure clock without waiting on bank financing or traditional buyer contingencies. For investors, pre-foreclosure investor strategies that focus on early outreach and quick due diligence consistently outperform waiting for auctions.

Private sales vs auctions: speed, price, and the risks for sellers

Let's talk about the trade-offs that Nebraska sellers face when deciding whether to sell privately during pre-foreclosure or let the property go to auction. The comparison is not as close as some people think.

| Comparison point | Pre-foreclosure private sale | Foreclosure auction |

|---|---|---|

| Seller equity recovered | Moderate to high | Low |

| Credit score impact | Minimal if sold | 100 to 150 point drop |

| Deficiency judgment risk | Negotiable | High |

| Closing timeline | 7 to 30 days | Day of auction |

| Seller involvement | Active, informed | None |

Auctions sell faster but at 20 to 40% below market, meaning pre-foreclosure private sales recover significantly more equity for sellers. On a $180,000 home, that gap could mean $36,000 to $72,000 less in your pocket at auction compared to a negotiated sale.

The risks of going to auction include:

- Deficiency judgments: If the auction price falls short of the loan balance, the lender may sue for the difference.

- No control over buyer: You have no say in who purchases, or at what price.

- Credit damage: A completed foreclosure stays on your credit report for seven years.

- Title complications: Buyers at auction sometimes inherit title issues, which can affect future transactions.

"The auction block is not a safety net. It is a last resort with real financial consequences."

For sellers using a distressed home sale guide, the message is consistent: a negotiated private sale, even at a discount, protects more of what you have worked for. If you are curious about buying at auction from an investor perspective, those deals do exist, but the risk profile is much higher and the due diligence window is essentially zero.

For most homeowners in Lancaster, Douglas, or Sarpy County, acting during pre-foreclosure is simply the smarter financial move.

Why acting early in pre-foreclosure is your strongest move

Here is our honest take after working with Nebraska homeowners in distressed situations: waiting almost never improves your outcome. We hear it often. "Maybe the bank will work with me." "Maybe the market will recover." "Maybe something will change." But every week of delay in pre-foreclosure costs you options.

The math is straightforward. A quick cash sale protects your credit, avoiding a 100 to 150 point score drop that affects your finances for years. A short sale takes 60 to 90 days and requires lender approval with no guarantee. An auction strips your equity and your control on the same day.

Even homeowners who are underwater, meaning they owe more than the home is worth, benefit from early action. Negotiating a short sale or cash sale early gives you leverage to minimize or eliminate deficiency judgments. Waiting removes that leverage entirely.

We have seen sellers in Omaha and Lincoln hold out hoping for a better offer, only to watch their legal window close and their options shrink to nothing. Acting through selling problem properties early is not giving up. It is making a smart financial decision under pressure.

The homeowner who calls a cash buyer on day 10 of default almost always walks away in a better position than the one who calls on day 150.

Need to sell fast? Nebraska pre-foreclosure experts can help

If you are a homeowner in Lancaster, Douglas, or Sarpy County facing pre-foreclosure, or an investor looking for off-market properties with real upside, Enko Home Buyers is built for exactly this situation.

We buy homes in Nebraska that need work, and we move fast. You can sell your Nebraska home fast without listings, showings, or waiting on bank financing. We make cash offers, handle the paperwork, and close on your timeline. If foreclosure is approaching, visit our page to stop foreclosure fast and learn how we can help you protect your credit and recover as much equity as possible. No pressure. No fees. Just a straightforward offer from a team that knows Nebraska.

Frequently asked questions

How long do pre-foreclosure sales usually take in Nebraska?

Pre-foreclosure homes in Nebraska often sell in as little as 7 to 21 days with cash buyers, but the legal window to act is typically 30 to 180 days. Cash buyers enable 7 to 21 day closings by skipping financing contingencies entirely.

What happens if a pre-foreclosure doesn't sell before the auction?

The property goes to auction where the homeowner loses control over price and walks away with little or no equity. Auctions recover 20 to 40% less than pre-foreclosure private sales for most sellers.

Why do investors prefer pre-foreclosure deals?

Investors favor pre-foreclosures because they can inspect the property, negotiate directly, and typically buy at a significant discount. 10 to 30% below market pricing on off-market homes needing renovation is the core appeal for cash buyers.

Can I stop a Nebraska foreclosure once the process starts?

Yes. You can sell during the pre-foreclosure period or negotiate directly with your lender to resolve the default. Nebraska's judicial process gives homeowners roughly 30 days after the notice of default to cure or sell before proceedings accelerate.